The Doctor House

May 10, 2021

The single decision most likely to work against attaining walkaway wealth is buying “too much house.”

Even unusually intelligent Americans, like physicians, tend to approach the economics of homeownership in a conceptual, not an analytical way. They tend to believe that real estate is a unique investment, ownership of which will inevitably result in building real wealth, and on which it is impossible to lose money in the long run.

None of this is true. Here are some key facts:

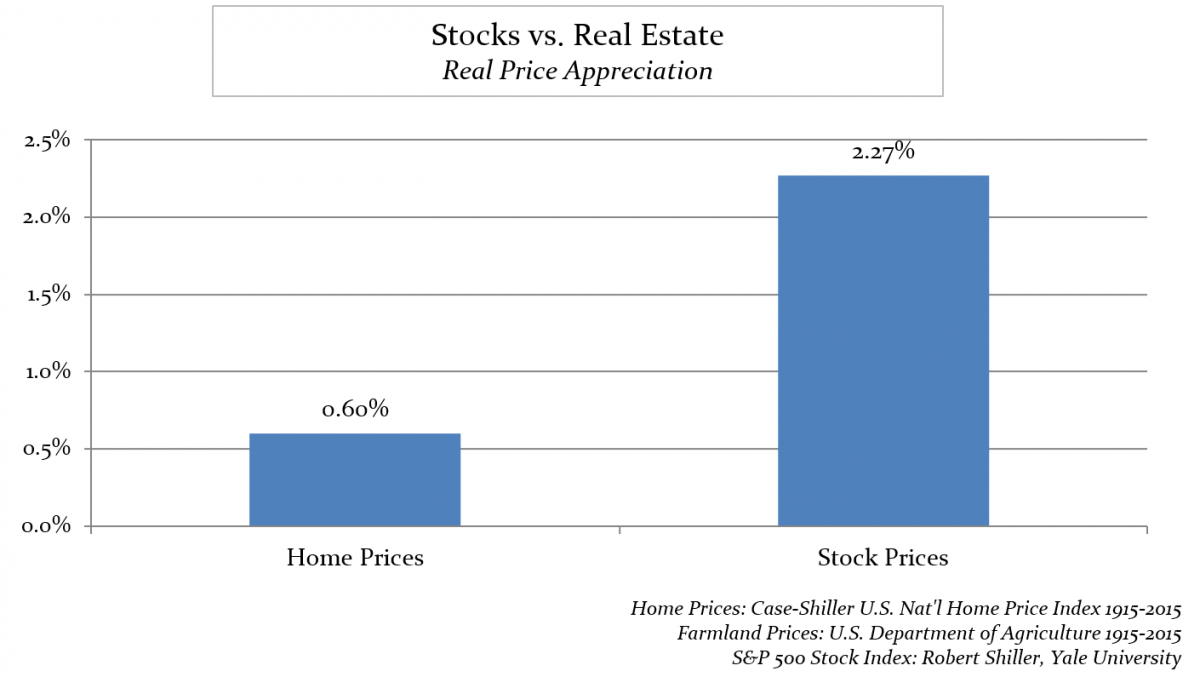

- Historically, houses have appreciated more slowly than equities. The best data on both asset classes comes from Nobel Prize-winning economist Robert Shiller of Yale University.1 The real (inflation-adjusted) price return on stocks has been more than three times higher than for houses. But this is only part of the story.

- Houses have costs, while stocks can produce dividends. Once you buy a house, your expenses have just begun. You must pay taxes, utilities, upkeep and maintenance, insurance.

- Much more than you expect, your house will also drive indirect costs. For example, if every other garage on the block contains a Porsche or Mercedes, it can be uncomfortable driving a used Toyota Camry. Status-signaling expenses like private school tuition, automobiles, even where you vacation, can actually be higher than the direct cost of owning your home.

Buy too much house, compound these differences in return and net cost over thirty years, and the difference in net worth at retirement will be profound. Avoiding becoming “house poor” is the single most important choice a new physician can make in her first three years of practice.

So should you rent instead of buying? Almost certainly not. At current interest rates, in most cities in the U.S., it still makes sense to buy instead of renting--if you plan to stay in your home for five or more years. (Over shorter periods, the transaction costs are likely to make a short-term house purchase unprofitable.)

All things being equal, for most higher-income earners it is economically better to buy your forever home than to rent it. But that does not mean that buying any home, regardless of size or cost, will be a financially superior choice to renting.

If you are renting a two-bedroom apartment, buying a two-bedroom condo is probably a smart decision. But if you move from that same apartment to a “starter home” that is 5,500 square feet and costs $1.5 million—a scenario we’ve seen more than once with young physicians—there is only the most remote chance that it will pay off in the form of higher net worth at retirement.

A beautiful house in a safe neighborhood can be one of life’s great joys. Almost every one of our clients owns their home. Just don’t confuse the expense of owning a home with a profitable investment asset.

-

Shiller won the Nobel Prize for his creation of the Shiller CAPE (Cyclically-Adjusted Price-Earnings), which established the systematic relationship between trailing inflation-adjusted earnings and forward stock market returns. Working with economist Karl Case of Harvard University and Wellesley College, he also co-created the Case-Shiller Housing Price Index, which tracks home prices in 20 metropolitan areas, released monthly by Standard & Poors.

- Log in to post comments